By any measure, the tax code is huge. According to Commerce Clearing House’s Standard Federal Tax Reporter it’s up to 74,608 pages in length.¹

And each Monday, the Internal Revenue Service publishes a 20- to 50- page bulletin about various aspects of the tax code.²

Fortunately, it’s not necessary to wade through these massive libraries to understand how income taxes work. Understanding a few key concepts may provide a solid foundation.

One of the key concepts is marginal income tax brackets.

Taxpayers pay the tax rate in a given bracket only for that portion of their overall income that falls within that bracket’s range.

Tax Works

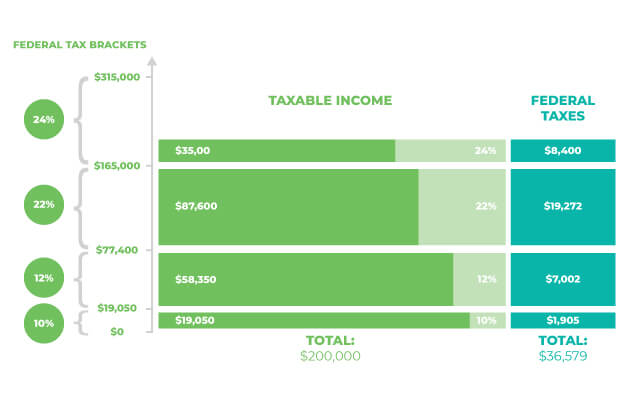

Seeing how marginal income tax brackets work is helpful because it shows the progressive nature of income taxes. It also helps you visualize how your total tax rate can be calculated. But remember, this material is not intended as tax or legal advice. Please consult a tax professional for specific information regarding your individual situation.

How Federal Income Tax Brackets Work

Say a married couple, filing jointly, in 2018, had a taxable income of $200,000. Each dollar over $165,000—or $35,000—would fall into the 24% federal income tax bracket. However, the couple’s total federal tax would have been $36,579—just under 20%, of their adjusted gross income.

This is a hypothetical example used for illustrative purposes only. It assumes no tax credits apply.

2018 Federal Income Tax Brackets

Your federal income tax bracket is determined by two factors: your total income and your tax-filing classification.

For the 2018 tax year, there are seven tax brackets for ordinary income — ranging from 10% to 37% — and four classifications: single, married filing jointly, married filing separately, and head of household.

- Washington Examiner, April 15, 2016. (Lastest data available.)

- Internal Revenue Service, 2018

![]()

Tip: High Bracket. In 1944, the highest federal income tax bracket was 94%. It applied to all income above $200,000 a year and applied to all taxpayers, regardless of filing status.

Tip: High Bracket. In 1944, the highest federal income tax bracket was 94%. It applied to all income above $200,000 a year and applied to all taxpayers, regardless of filing status.

Source: Tax Policy Center, 2017

Fast Fact: First Brackets. In 1913 — immediately after the 16th Amendment gave Congress the power to levy taxes on income — the government set up a system of seven federal income tax brackets with rates ranging between 1% and 7%. Less than one in 100 people had to pay even the lowest rate.

Fast Fact: First Brackets. In 1913 — immediately after the 16th Amendment gave Congress the power to levy taxes on income — the government set up a system of seven federal income tax brackets with rates ranging between 1% and 7%. Less than one in 100 people had to pay even the lowest rate.

Source: OurDocuments.gov, 2017; IRS, August 6, 2017

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2019 FMG Suite.