According to Giving USA 2017, Americans gave an estimated $390.05 billion to charity in 2016. That’s the highest total in more than 60 years since the report was first published.1

Americans give to charity for two main reasons: To support a cause or organization they care about, or to leave a legacy through their support.

When giving to charitable organizations, some people elect to support through cash donations. Others, however, understand that supporting an organization may generate tax benefits. They may opt to follow techniques that can maximize both the gift and the potential tax benefit. Here’s a quick review of a few charitable choices:

Direct gifts are just that: contributions made directly to charitable organizations. Direct gifts may be deductible from income taxes depending on your individual situation.

Charitable gift annuities are not related to annuities offered by insurance companies. Under this arrangement, the donor gives money, securities, or real estate, and in return, the charitable organization agrees to pay the donor a fixed income. Upon the death of the donor, the assets pass to the charitable organization. Charitable gift annuities enable donors to receive consistent income and potentially manage taxes.

Pooled-income funds pool contributions from various donors into a fund, which is invested by the charitable organization. Income from the fund is distributed to the donors according to their share of the fund. Pooled-income funds enable donors to receive income, potentially manage taxes, and make a future gift to charity.

Gifts in trust enable donors to contribute to a charity and leave assets to beneficiaries. Generally, these irrevocable trusts take one of two forms. With a charitable remainder trust, the donor can receive lifetime income from the assets in the trust, which then pass to the charity when the donor dies; in the case of a charitable lead trust, the charity receives the income from the assets in the trust, which then pass to the donor’s beneficiaries when the donor dies.

Using a trust involves a complex set of tax rules and regulations. Before moving forward with a trust, consider working with a professional who is familiar with the rules and regulations.

Donor-advised funds are funds administered by a charity to which a donor can make irrevocable contributions. This gift may have tax considerations, which is another benefit. The donor also can recommend that the fund make distributions to qualified charitable organizations.

Some people are comfortable with their current gifting strategies. Others, however, may want a more advanced strategy that can maximize their gift and generate potential tax benefits. A financial professional can help you assess which approach may work best for you.

Remember, the information in this article is not intended as tax or legal advice. And it may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

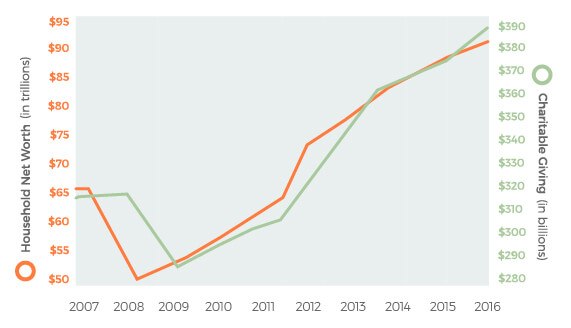

Giving and Net Worth

Charitable giving appears to trail household net worth by about one year. When household net worth dipped in 2008, charitable giving dipped in 2009.

Chart Source: Giving USA Foundation, 2017; Federal Reserve, 2017

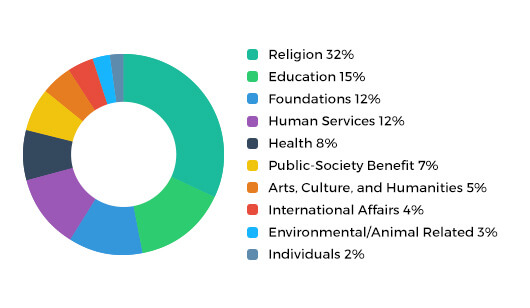

Where the Money Goes

The biggest percentage of charitable contributions — 32% — went to churches and religious organizations. A variety of different types of groups were on the receiving end of charitable gifts.

Chart Source: Giving USA Foundation, 2016

![]()

Tip: Importance of Itemizing. Charitable contributions are deductible only if you itemize deductions on Form 1040, Schedule A. Those who take the standard deduction cannot deduct their contributions.

Tip: Importance of Itemizing. Charitable contributions are deductible only if you itemize deductions on Form 1040, Schedule A. Those who take the standard deduction cannot deduct their contributions.

Internal Revenue Service, 2017

Fast Fact: Contributions by individuals, couples, and families accounted for 72% of the $390.05 billion donated to charitable organizations in 2016.

Fast Fact: Contributions by individuals, couples, and families accounted for 72% of the $390.05 billion donated to charitable organizations in 2016.

Giving USA Foundation, 2017

- Giving USA Foundation, 2017

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. Some of this material was developed and produced by FMG, LLC, to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security. Copyright 2019 FMG Suite.